Infrastructure outsourcing: Unlocking returns via scaled leasing

Key takeaways

-

Ownership model shifts. Capital intensity and operational complexity are driving a shift from asset ownership to leasing and third‑party ownership models, expanding the opportunity set for infrastructure investors.

-

Built like infrastructure. Equipment leasing platforms can offer core infrastructure characteristics, with long-term contracted revenues backed by essential assets and aligned with structural macro drivers. Their smaller scale creates capacity for faster growth and potentially higher returns.

-

Pressures driving change. Increased electrification needs, tighter regulation and competitive supply chains are compounding simultaneously, creating capital demands that many service operators simply cannot meet from their own balance sheets.

Infrastructure operators are increasingly separating ownership from operations to enhance flexibility and support long-term growth, unlocking attractive opportunities for institutional investors in scaled infrastructure leasing platforms.

Electrification mandates and tighter regulation are driving higher capital requirements across infrastructure markets, even as post‑COVID margin pressures persist. Rising equipment costs are making balance sheets harder to defend and ownership harder to justify for many operators. Leasing offers operators a practical way to maintain flexibility and keep pace with technological change without committing scarce capital.

Operators are increasingly leasing critical machinery and outsourcing maintenance to scaled specialists that can buy, manage and redeploy assets more efficiently.

Large lessors bring scale and purchasing power that individual operators cannot match, resulting in a total cost of ownership around 10% lower, in some cases, than self-ownership while also spreading payments over time. For many operators whose credit profiles were weakened during COVID, infrastructure leasing has become less of a preference and more of a requirement.

For investors, leasing platforms can combine the resilience typically associated with traditional infrastructure with the potential for higher returns through active management. While cash flows are underpinned by essential services and long‑term, inflation‑linked contracts, the leasing platforms themselves are often smaller and less mature, offering runway for growth as infrastructure outsourcing accelerates and ownership continues to consolidate.

What’s fueling the shift to infrastructure outsourcing?

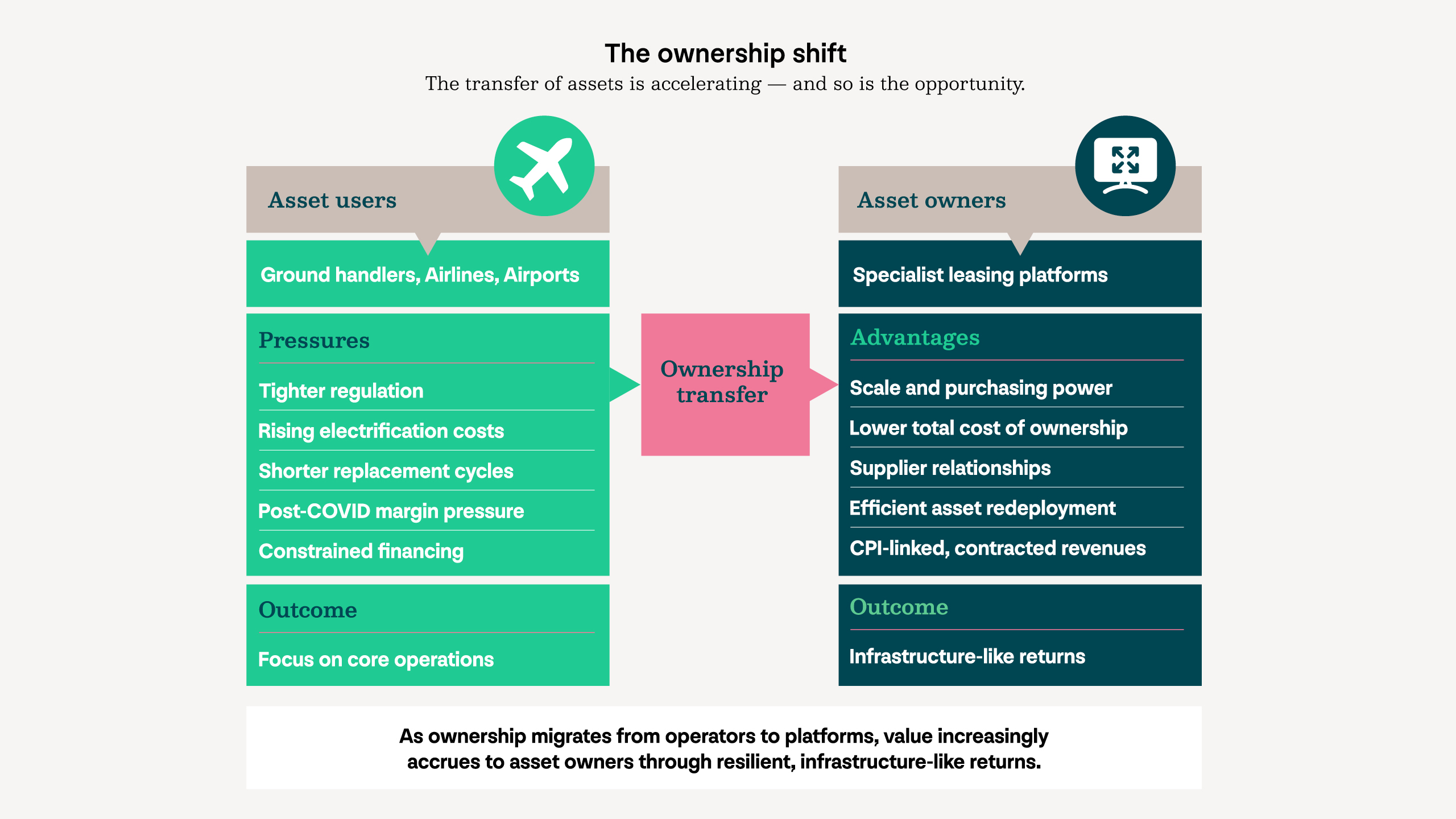

Across a growing range of infrastructure sectors and geographies, outsourcing infrastructure asset ownership and maintenance is moving from occasional to mainstream. The shift reflects a convergence of operational, financial and structural pressures that are accelerating its adoption across air transport, rail, ports and other asset-intensive services.

Operationally, outsourcing allows service providers to focus on what they do best. Infrastructure businesses are increasingly required to manage complex fleets of regulated, technologically advanced equipment across multiple sites and jurisdictions. Transferring ownership and maintenance to specialist lessors reduces that complexity, freeing management teams to concentrate on performance, safety and customer outcomes rather than capital allocation.

Balance sheet flexibility is an equally powerful driver. Owning critical equipment requires significant upfront capital costs, often with assets that extend well beyond underlying service contracts. Leasing offers a more practical alternative, allowing operators to match contract length with service agreements, while reducing capital intensity and preserving financial resilience. For many operators facing tighter credit conditions, this flexibility can be increasingly important.

Figure 1. The ownership shift

The transfer of assets is accelerating — and so is the opportunity.

Post-COVID supply chain disruption has further strengthened the case for infrastructure outsourcing.

Equipment shortages and constrained manufacturer capacity have made self-sourcing increasingly inefficient and costly. Scaled leasing platforms, backed by established supplier relationships and significant purchasing power, are often better positioned to secure and maintain assets at speed. Individual operators, by contrast, can face delays of 12 to 24 months in some sectors for new equipment, which creates operational risk and service disruption. From there, rising capital intensity is adding further pressure.

These dynamics point to a structural shift rather than a cyclical response. As asset costs rise, regulation tightens, and operational complexity increases, ownership is migrating toward specialist leasing platforms that can manage capital and scale more efficiently, reshaping how infrastructure-adjacent services are delivered in the process.

As of May 2026, the drivers underpinning outsourcing are not only persistent, but they are intensifying. Electrification and regulation are joining forces to create significant capital requirements across numerous infrastructure sectors, requirements that many service businesses are unable to absorb.

Electrification is a central catalyst for the trend in infrastructure outsourcing. Across the transport sector, for example, regulators are mandating the replacement of diesel equipment with electric alternatives to reduce emissions. While supportive of long-term sustainability goals, this transition can materially increase fleet costs. Electric machinery embeds higher levels of technology and, as a result, often carries a much higher upfront price than legacy diesel assets.

Regulatory change is compounding this further by shortening replacement cycles. In parts of Europe, critical airport equipment must now be replaced within 10-15 years, compared with historical lifecycles of 20 to 25 years. This accelerates reinvestment requirements and raises ongoing capital intensity at precisely the moment margins remain under pressure. For many operators, the scale and pace of required fleet renewal simply exceeds available balance sheet capacity.

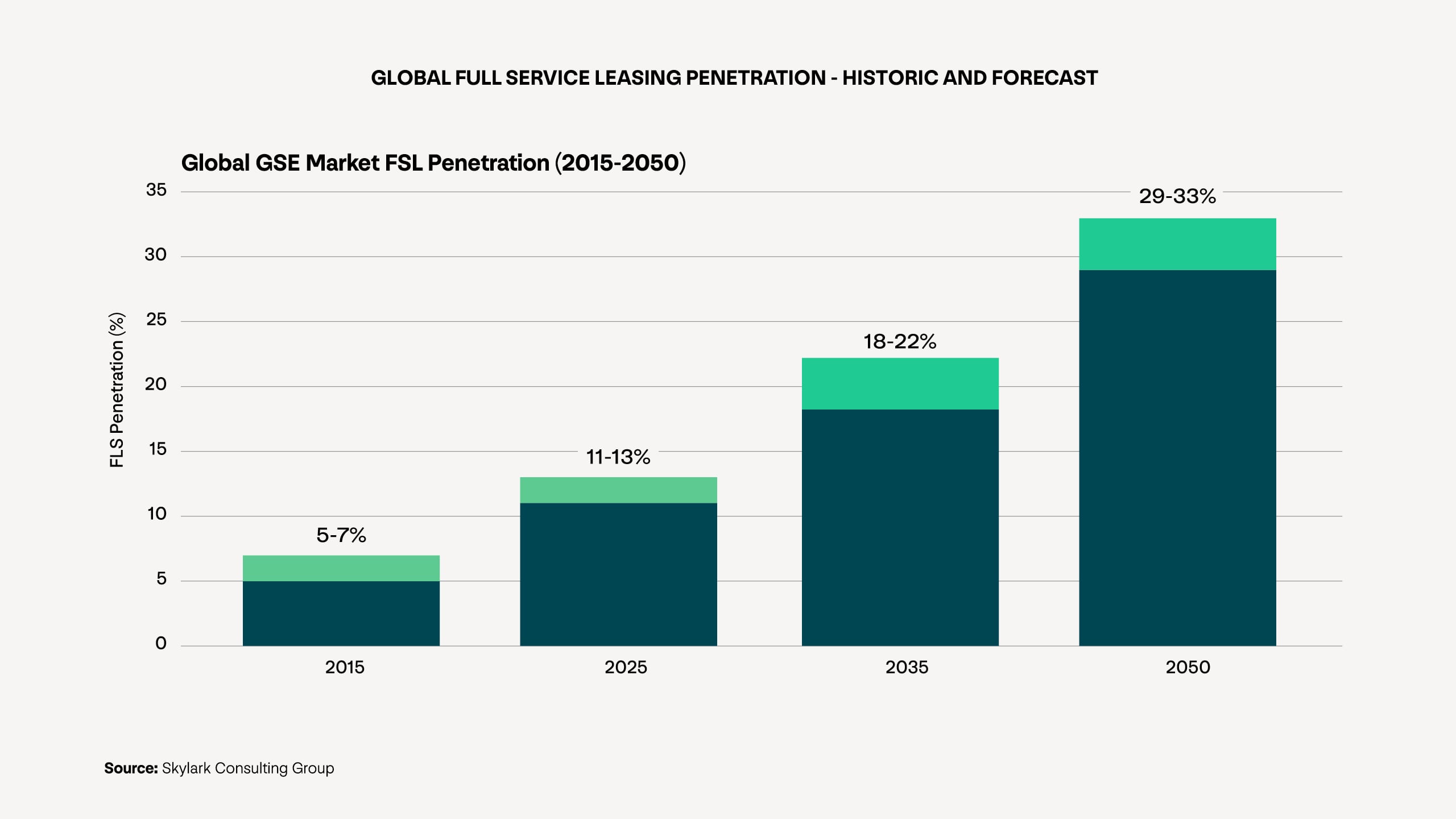

The evidence reflects this. In airport ground support equipment (GSE), leased penetration in markets have risen materially over the past decade, illustrating how quickly structural economics can reshape ownership models. This trend is likely to accelerate as cost and regulatory pressures intensify across markets.

Figure 2. Global FSL Penetration - Historic and Forecast

Global GSE Market FSL Penetration (2015-2050)

Adoption is not uniform, however. Because these assets are critical to day‑to‑day operations, many service providers remain cautious about outsourcing and the perceived loss of control, resulting in a more gradual transition for some operators.

Asset ownership exhibits infrastructure‑like characteristics

For investors, this trend in infrastructure outsourcing creates a growing and durable opportunity in equipment leasing and asset ownership platforms. Many of these businesses sit deep within the supply chains of essential infrastructure systems, which provide the ground support equipment that keeps airports running, the handling machinery that moves cargo through ports, and the maintenance fleets that service rail and utility networks. While individually smaller than traditional infrastructure assets they serve, they are no less critical to day-to-day operations.

These businesses benefit from long-term customer relationships, asset-centric operating models, CPI-linked revenues, and exposure to those same essential systems.

Globally, for GSE, outsourcing has jumped from ~6% in 2015 to ~12% in 2025, a number that will continue to climb.

At the core of this opportunity is the predictability of leasing cash flows. Equipment leasing platforms typically operate under long‑term contracts that align closely with the service agreements held by their customers. In sectors such as air transport, ground handling and other infrastructure services, these businesses sit directly within the supply chains of large-scale infrastructure assets. Leasing agreements are structured to match these tenors, creating contracted, visible revenues that are directly linked to the ongoing operation of essential infrastructure.

Within the equipment leasing segment, specialized platforms with strong maintenance capabilities can be particularly resilient, typically exhibiting stronger moats and unit economics than generalist lessors facing increased competition and customer churn.

CPI‑linked pricing can further enhance cash flow stability. As replacement costs rise, inflation linkage helps preserve real returns and reduces the risk of margin erosion over time. This feature is particularly valuable in asset‑intensive environments where costs adjust faster than revenues and where capital reinvestment cycles are shortening.

The essential nature of the underlying services also supports payment durability. Equipment such as ground support vehicles, baggage handling systems, and transport fleets is mission‑critical to day‑to‑day operations. As a result, lease payments are typically prioritised, even during periods of operational or financial stress, reinforcing the resilience of contracted cashflows.

Predictability is supported not only by contracts but by the assets themselves. Post‑COVID supply‑chain disruption has created persistent equipment shortages, increasing the redeployment value of well‑maintained assets. If a contract ends, assets can often be re‑leased or redeployed more efficiently than sourcing new equipment, limiting downtime and supporting continuity of cash generation.

For institutional investors, the opportunity is compelling. Equipment leasing and asset ownership platforms can offer contracted revenues, inflation linkage, and asset resilience that mirror core infrastructure—backed by essential services operators cannot afford to interrupt. As these forces intensify, the flow of capital from constrained operators to scaled, well-capitalised platforms are set to deepen.

If you would like to discuss how these cyclical changes may impact your portfolio, please visit our contact page and complete the form, and a member of our Global Client Solutions team will be in touch.

For full details, including all disclaimers applicable to the data contained herein, please refer to the complete article.

Josh Crane

Josh is responsible for advancing IFM’s investment activities in Australia and Asia-Pacific, covering the origination and execution of transaction opportunities and managing platform investments.

Thomas Yates

Thomas Yates is a Senior Associate in Infrastructure who joined IFM Investors in January 2024. He is involved in infrastructure origination, transactions and asset management, with a focus on investment analysis, market research, and the preparation of investment proposals and investor reporting.

Related articles

The mid-market advantage in infrastructure investing

APAC private credit: A diversifier for global portfolios

Power demand back to growth. But is the grid ready?