Reducing carbon exposure in core equity portfolios

How does IFM approach low carbon investing for core equity portfolios?

Laurence Irlicht:

One of the most straightforward approaches that investors can take to align their portfolios to the low carbon future is to lower the exposure to carbon.

At IFM, we do this for clients by optimising the portfolio’s positions to achieve the desired level of carbon reduction, whilst minimising the risk against the index (tracking error).

Some of the strategies we use to reduce carbon exposure include:

-

Reducing exposure to Scope 1 and 2 emissions1

-

Controlling exposure to fossil fuel reserves to reduce stranded assets exposure

-

Stock and sector exclusions

IFM has been running low carbon portfolios since 2012, and now does so across both Global and Australian equities.

The benefits include a measurable reduction in carbon exposure, increased capital flows to ’cleaner’ companies and the potential to lower exposure to carbon pricing in the event that it becomes a material cost.

Research suggests that reducing carbon exposure is easier in global equity portfolios than Australian portfolios – can you explain why?

David Welch:

Most scope 1 and 2 carbon emissions are generated by three sectors: Utilities, Energy and Materials. So reducing carbon exposure is primarily achieved by stock selection within these sectors and allocating away from these sectors.

Companies in the Utilities sector generate the highest carbon emissions, with the sector having a Weighted Average Carbon Intensity (WACI) of over 2,000 in MSCI World ex Australia benchmark as of March 2021. The Energy and Materials sectors also have high WACIs (472 and 659 respectively), both well above the overall index WACI of 97.

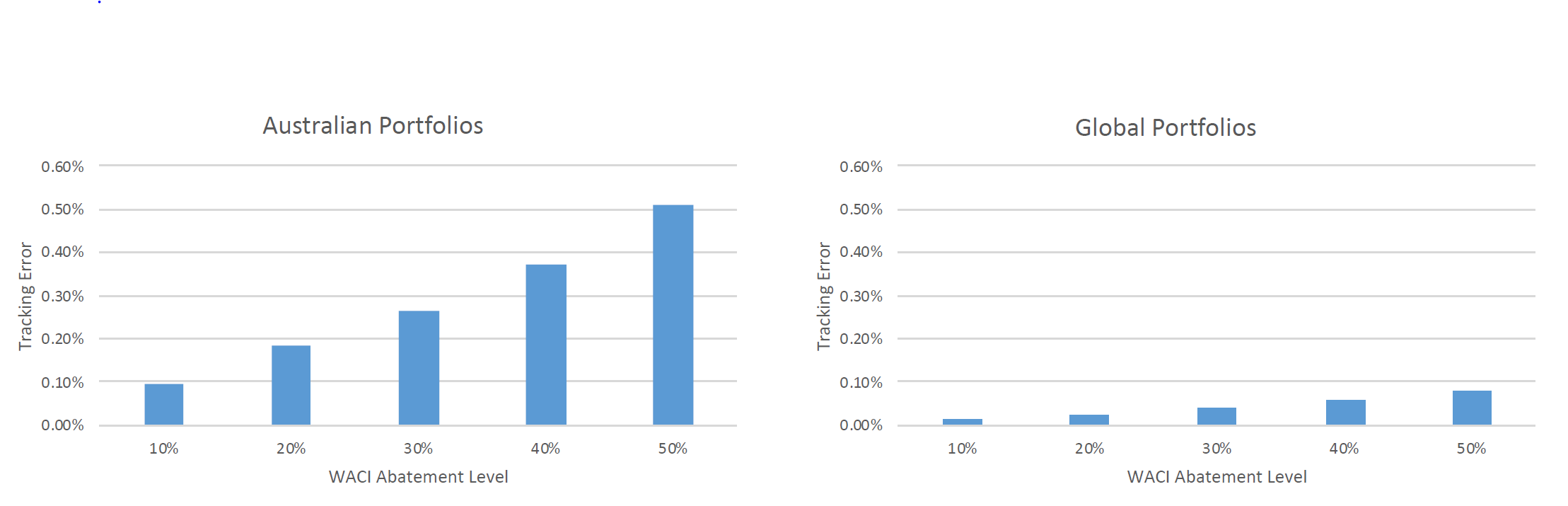

The global benchmark has more stocks and a broader range of carbon emissions than the Australian benchmark, making it possible to achieve greater reductions in global carbon exposure for lower levels of tracking error as shown in Figure 1.

Figure 1 - Abatement levels and tracking error

Source: MSCI, IFM Investors

The global benchmark has 27 stocks with very high carbon emissions – all have a WACI over 3,000 and the highest is over 11,0002. A small reduction in exposure to these stocks can achieve quite large reductions in carbon exposure for a relatively small increase in tracking error. By contrast, the S&P/ASX 100 Index has only two stocks with a WACI over 3,000 and the highest is only just over 4,500. So larger active positions are required to achieve the same level of carbon reduction in the Australian market.

In the global benchmark there are also more stocks in the high carbon emitting sectors that have very low levels of carbon emissions. This is especially true within the Utilities sector given the focus on clean energy generation. These stocks can be held above benchmark weight, enabling a reduction in carbon exposure without sector bias.

The Australian benchmark currently lacks ‘clean’ utilities, hence allocation away from the sector is often implemented to reduce carbon exposure. So Australian low carbon portfolios end up with higher levels of sector bias, compared to global portfolios, which contributes to higher tracking error.

What types of low carbon equity strategies does IFM offer?

Laurence Irlicht:

IFM can work with clients on both “off the shelf” low carbon strategies and bespoke solutions, depending on the individual client’s needs.

’Off the shelf’ strategies may be quick and easy to implement, however investors have to accept whatever risk and carbon reduction parameters are specified by the strategy. Bespoke solutions can better address an investor’s specific carbon reduction goals and can also include other objectives, such as targeting companies that are involved in the transition to a low carbon economy.

Bespoke solutions can also be adjusted over time as an investor’s climate goals evolve. Whilst bespoke solutions take longer to implement and require more in-depth analysis in the initial stages, for investors with specific climate related goals, this is likely to be time well spent!

What do you do beyond low carbon?

Laurence Irlicht:

Beyond low carbon, it is possible to target companies that have greater resilience to climate change, or those compatible with a low global temperature rise. We also manage portfolios targeting a range of ESG objectives or alignment with the Sustainable Development Goals.

The objective is to meet each investors’ individual needs. It’s really fun when an investor comes to us with their own specific requirements, and we work in partnership to create a strategy that is designed to best meet their needs.

We think it is this partnership approach that really sets us apart.

1 Scope 1 emissions are direct emissions from owned or controlled sources. Scope 2 are indirect emissions from the generation of purchased energy. Scope 3 emissions are all indirect emissions (not included in scope 2) that occur in the value chain of the reporting company, including both upstream and downstream emissions - https://ghgprotocol.org/sites/default/files/standards_supporting/FAQ.pdf. We are also actively researching lowering Scope 3 emissions too.

2 As at 31 March 2021.

Laurence Irlicht

Laurence leads the IFM Listed Equities Quant team. This team is currently focused on research and portfolio management for ESG, Climate change/Low Carbon and Factor strategies. Laurence’s previous roles have included Investment Director Quantitative Analysis at the Victorian Funds Management Corporation; Investment Director (Asset Allocation) at Westpac Investment Management; and Senior Portfolio Manager at Rothschild Australia.

David Welch

With more than 10 years industry experience, David undertakes research activities and develops and manages the firm’s equity ESG and enhanced indexed strategies. Prior to joining IFM Investors, David worked at IOOF as a Portfolio Analyst.

Related articles

The mid-market advantage in infrastructure investing

APAC private credit: A diversifier for global portfolios

Power demand back to growth. But is the grid ready?