Key takeaways

- The private credit market is exhibiting increasing signs of strain. Years of unchecked inflows have shifted leverage toward borrowers, eroded investor protections, and left returns increasingly dependent on refinancing conditions rather than the quality of underlying assets. As volatility rises, the gap between perceived yield and actual risk is widening. To that point, redemption risk is now a meaningful concern, with several large vehicles in early 2026 facing withdrawal requests that exceeded standard quarterly limits.

- Investors are responding by moving toward more defensively structured alternatives. Infrastructure debt stands out: strong structural protections, robust collateral packages, and historically higher recovery rates (70-85%)1.

- Geography matters too. Private credit markets in the US and Europe are crowded, with compressed spreads and weakened covenants. Asia-Pacific presents a different picture — less saturated, more conservatively structured, and underpinned by lower leverage and stronger lender protections. For investors seeking discipline and diversification as risks build elsewhere, it represents a compelling alternative.

Private credit challenges

The private credit industry, now totaling $2.2 trillion in assets and growing2, is coming under increasing pressure as the conditions that supported its rapid growth have fundamentally changed. Driven by strong investor demand for yield and the pullback of traditional bank lending following post-GFC regulatory reforms, private credit funds stepped in to fill the gap, benefiting from greater underwriting flexibility and a willingness to finance borrowers that traditional lenders were less inclined to support. Fundraising momentum remained strong through 2025, with approximately $224 billion raised globally3, underscoring the scale the market has now reached.

That scale is reshaping the asset class and creating new pressures. Significant capital inflows have led to overcapitalization in core strategies, intensifying competition and compressing spreads. As capital chased deployment, underwriting standards weakened in some areas and lender protections eroded.

As a result, redemption requests are a real concern. In early 2026, several large private credit vehicles faced withdrawal requests that exceeded standard quarterly limits, with some funds gating redemptions, others temporarily raising caps, and at least one committing firm capital to support liquidity. This series of events has drawn wider attention to liquidity mismatches in certain fund structures and how managers value and report their portfolios.

One of the clearest expressions of this shift has been the growing use of payment-in-kind (PIK) interest, which allows borrowers to defer cash interest by capitalizing it into principal. While PIK can provide near-term liquidity relief, it increases leverage, delays the recognition of stress, and shifts return outcomes toward refinancing rather than sustainable cash flow generation. According to Lincoln International, 11% of private loans paid PIK income in the fourth quarter of 2025, a share that could rise further as refinancing pressure builds4.

For Business Development Companies (BDCs), PIK introduces an additional structural challenge. Under SEC regulations, BDCs must distribute at least 90% of taxable income annually, including non-cash items such as PIK interest, creating potential cash-flow imbalances during periods of borrower stress. Alongside this, borrower‑friendly documentation has become more prevalent, allowing for looser covenants and EBITDA adjustments to mask true leverage.

Private credit default rates

Consequently, credit stress is now surfacing more frequently. According to Fitch Ratings, private credit default rates increased to approximately 5 to 6% in early 2026, compared with 1 to 3% during the 2015 to 2021 period, with some portfolios reporting rates as high as 9% in 20255. Fitch also recorded 74 unique borrower defaults over the past 12 months, including 11 in February 2026 alone6.

In fact, these statistics may even understate underlying credit stress, reflecting practices such as amend-and-extend restructurings and delayed write-downs, alongside manager discretion in how impairments and valuations are classified. At IFM, infrastructure debt loans are valued using fair market value and defaults are classified under Moody’s definition, with a separate restructuring metric to provide a more transparent and conservative view of portfolio performance.

These pressures are amplified by portfolio concentration in technology and software borrowers, many of which lack tangible collateral and are underwritten on recurring-revenue assumptions. The rapid rise of AI has further intensified competition and increased revenue volatility across these sectors. As scale meets a turning credit cycle, structural and cyclical pressures are converging, placing the private credit market under increasing strain.

Safety Infrastructure Debt Can Offer

We believe infrastructure debt remains less crowded and offers a differentiated risk-return profile relative to broader corporate private credit markets. As private credit participants continue pulling back amid rising stress, the number of active lenders may decline and credit spreads may widen, creating opportunities for established infrastructure managers such as IFM to deploy capital on more attractive terms.

Infrastructure projects typically benefit from defensive characteristics such as regulated frameworks, long-term contracted revenue streams, and essential service demand, contributing to more predictable cash flows. Additionally, infrastructure loans generally include strong structural protections, robust collateral packages, and historically higher recovery rates (70-85%)7. Reflecting the essential nature and hard backing of the underlying assets, we believe infrastructure borrowers tend to exhibit lower sensitivity to economic cycles, interest rate volatility, and technological disruption than corporate private credit borrowers.

IFM focuses on senior-secured investments that typically exhibit monopolistic characteristics, low demand risk and financial safeguards. We aim to structure investments with robust security packages and restrictive covenants to help support recovery potential and manage downside risk. Cash sweeps are typically implemented to reduce debt at maturity through excess cash flow and mandatory amortizations, thereby mitigating refinancing risk. During credit stress, reporting requirements and covenants serve as early warning triggers, provide liquidity buffers and strengthen creditor protections and recovery rates. As market volatility persists, we believe infrastructure debt’s defensive attributes position it as an alternative within the broader private credit universe and a resilient and “all-weather” investment private markets strategy.

Infrastructure projects typically benefit from:

Infrastructure loans generally include:

Infrastructure borrowers tend to exhibit:

Diversification through Asia-Pacific Private Credit

The Asia-Pacific (APAC) private credit market, which we believe benefits from strong regional economic fundamentals, can offer another diversification alternative from the crowded U.S. and European markets.

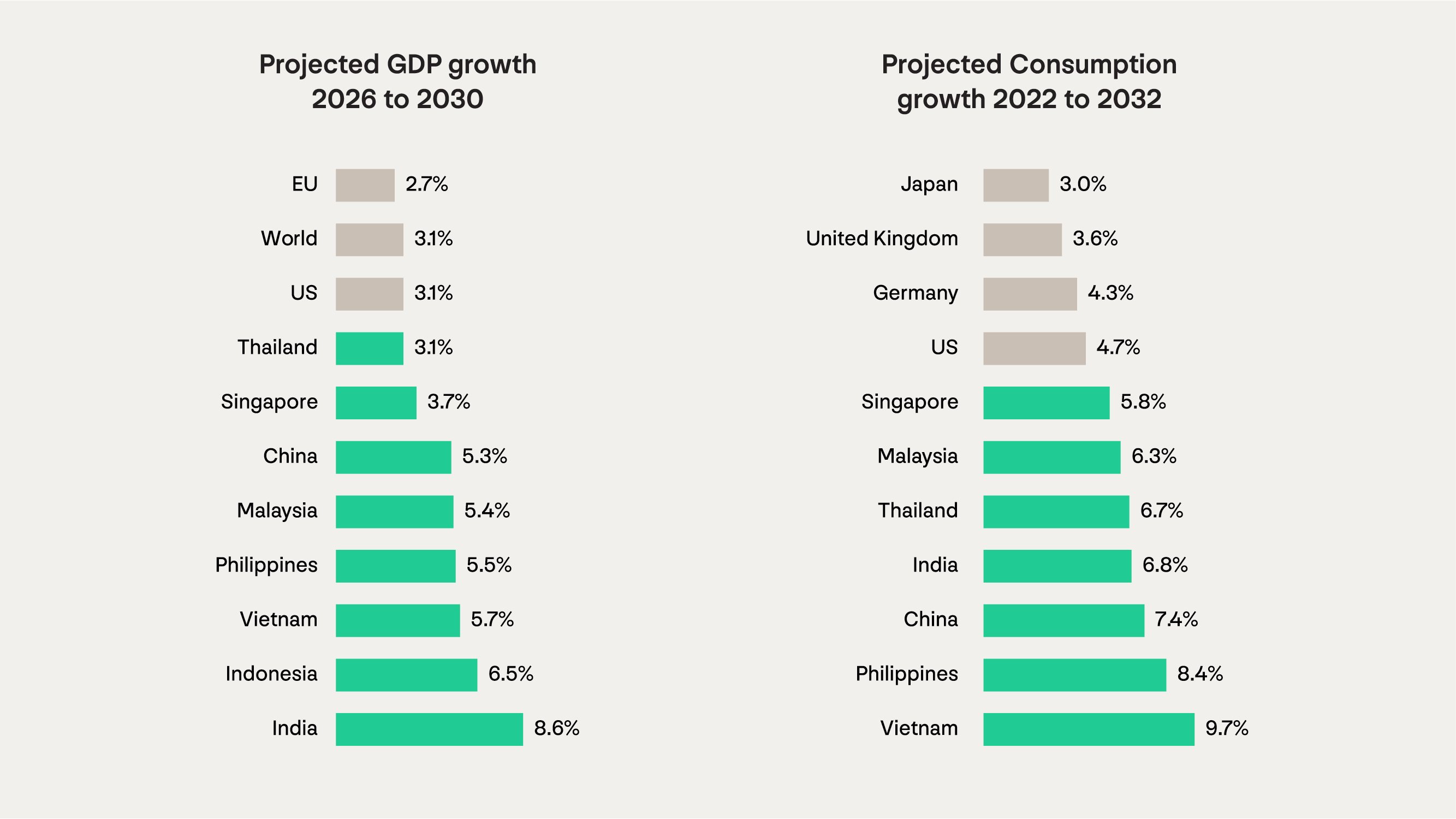

APAC’s private credit market is projected to grow from ~$60 billion today to ~$92 billion by 2027, representing a ~16% compound annual growth rate (CAGR) from 20248. APAC accounts for nearly 50% of global GDP, and GDP growth - driven significantly by South and Southeast Asia and is projected to remain steady, with a CAGR of approximately 4-5% through 2030, compared to approximately 3.1% for the U.S. and 2.7% for Europe.

APAC capital markets also remain relatively less developed, offering private credit investors access to attractive yield potential, structural growth and meaningful diversification. Unlike the U.S., where bank disintermediation accelerated post-GFC and the market has become highly competitive and increasingly commoditized, APAC remains significantly bank dominated.

Many of the U.S. private credit market’s current challenges stem from its rapid growth, which has contributed to the gradual erosion of the structural fundamentals that initially underpinned the asset class’s appeal. With the US market’s weakening lender protections, increasing PIK interest, and elevated software sector exposure, APAC offers a developing private credit market characterized by:

-

Conservative leverage

-

Stronger covenants and collateral coverage

-

Limited PIK exposure

-

Lower software concentration

APAC private credit returns are primarily driven by cash yield, enhanced by illiquidity and complexity premiums and relatively wider credit spreads. Additionally, deal flow is not solely dependent on sponsor-backed lending, opportunities span a broad range of borrowers and sectors, providing greater diversification and more consistency. With historically low correlation to U.S. and European credit markets, APAC private credit provides investors with a lower-risk entry point into the region and exposure to a lender-friendly market with a growing demand for private capital.

With more than 25 years of investing experience in APAC private credit, we believe IFM is well positioned to be a leading non-bank lender in the region. We aim to focus on senior secured debt directly sourced opportunities, targeting borrowers with resilient business models and structuring loans with conservative terms and strong lender protections, while avoiding PIK interest structures. We also seek to provide investors access to a range of industries not widely accessible in the U.S. and Europe, including manufacturing, textiles, and precision engineering.

IFM has been an early-stage mover in the region across the private credit spectrum, including corporate, real estate, infrastructure and structured financing. We were one of the first non-bank lenders via warehouse financing in Australia, and are currently one of the largest warehouse mezzanine providers, and a top two participants in Australian securitization. This scale and presence can provide IFM with strong deal flow and the ability to capitalize on opportunities across market cycles in APAC’s underbanked credit markets. As the global economy further fragments and bank lending dynamics evolve, we believe APAC can offer portfolio diversification and access to generally stable long-term growth opportunities supported by strong structural tailwinds.

For full details, including all disclaimers applicable to the data contained herein, please refer to the complete article.

[1] World Bank. Financial performance of infrastructure investment. September 11, 2024.

[2] Moody’s. “Private credit outlook 2026 executive summary” January 21, 2026.

[3] S&P Global. “Global private credit fundraising increased in 2025” January 7, 2026.

[4] iCapital, Advisor Manual: A Practical Guide to Evaluate Conservatism in Private Credit, February 25, 2026.

[5] Reuters. “US private credit defaults hit record 9.2% in 2025, Fitch says,” March 6, 2026.

[6] Bloomberg, “Pimco Says Private Debt Should Face ‘Full-Blown Default Cycle’,” March 6, 2026.

[7] World Bank. Financial performance of infrastructure investment. September 11, 2024

[8] The Business Times, Apac private credit to reach US$92 billion in 2027 on wealth boom,” October 30, 2025. Apac private credit to reach US$92 billion in 2027 on wealth boom

Meet the authors

Rich Randall

Rich is responsible for the creation and management of IFM Investors’ debt investments strategies and portfolios, and for the debt investments team globally. He also heads IFM Investors’ North American debt investment business. Based in New York, Rich has more than 20 years of experience in originating, analysing, structuring and arranging debt facilities for large infrastructure projects.

Hiran Wanigasekera

Hiran is an Executive Director and Co-Head of IFM Investors' APAC Diversified Credit capability. He responsible for joint management of key credit portfolios, credit product strategies and managing the day-to-day running of debt portfolios. Hiran has worked across a wide range of credit sectors and industries including bank lending, corporate credit and structured investments.

Jonny Bezalel

Jonny is a Vice President in our Global Client Solutions team, serving as the North American Product Specialist for infrastructure debt. In this role, he supports both existing client relationships and prospective investor engagements.

Hadley Murphy

Hadley is an Analyst on our Global Client Solutions team, serving as the North American Product Specialist for infrastructure debt. In this role, she supports both existing client relationships and prospective investor engagements.

Related articles

Where investment decisions can fall short – and why

Beyond data centres: Could fibre optic networks bridge the AI divide?

Infrastructure: The times they are a-changin’