Key takeaways

-

Asia-Pacific private credit is at an inflection point, with the market growing nearly fourfold from a low base over the past 15 years.

-

Regional growth expected to outpace other developed economies and structural financing gaps may create sustained demand, offering potential opportunities for investors wishing to geographically diversify their exposure.

-

The region accounts for a disproportionate share of global GDP growth, but remains significantly underrepresented in global portfolios.

Amid public market volatility, thematic shifts in capital allocation favouring lower-volatility assets and an increasing focus on diversification, the next chapter of private credit is being written, not in New York or London but across the Asia-Pacific (APAC) region.

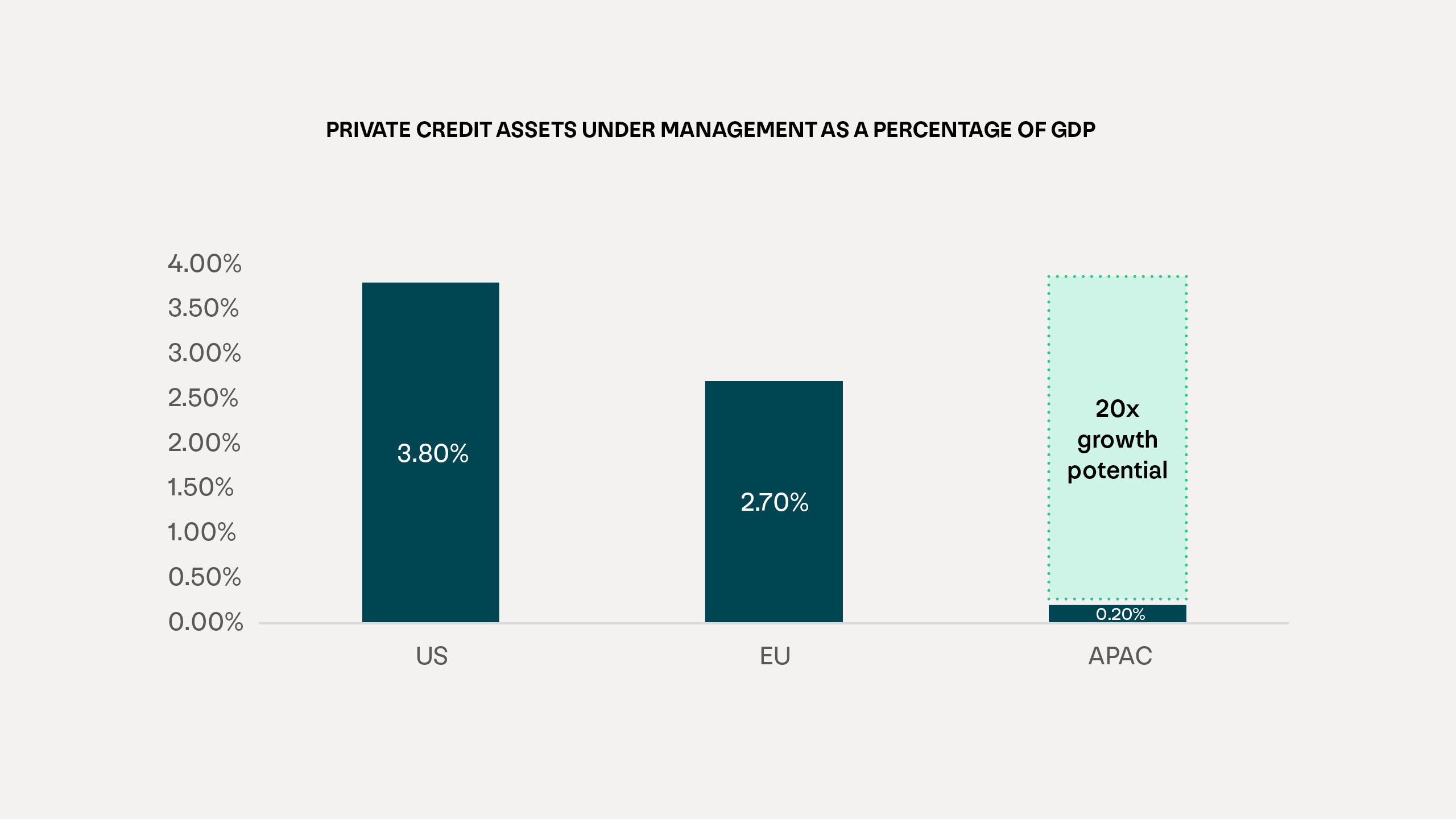

The size of the private credit market in APAC has increased nearly fourfold in the last 15 years, with assets more recently standing at US$59 billion in 2024 and expected to exceed US$91 billion by 2027 – equivalent to annual growth of 16% over three years[1]. The growth projections may be eye-catching, but more important is the opportunity this growth represents. Compared to the mature markets in the US and European Union, private credit penetration in APAC remains woefully low. Additionally, we believe that traditional bank lending, while still the dominant way for companies to access loans, is restrictive and inefficiently allocates capital. Continued growth in APAC private credit as seen in recent years could see it becoming an essential capital source for fuelling further economic growth – marking an inflection point. It is arguably an increasingly compelling asset class with a promising outlook, one that can bring key structural benefits to global portfolios.

Figure 1 - Private credit assets under management as a percentage of GDP

Source: International Monetary Fund DataMapper, data as at World Economic Outlook October 2025

The APAC growth story

The International Monetary Fund projects APAC will be the primary growth engine for the world economy for decades to come, with the region last year predicted to contribute approximately 60% of global growth[2]. Additionally, the region’s growth is comfortably expected to outpace developed markets in coming years, with APAC expected to grow 4-4.5% per annum to 2027, compared to only 1.5% for Europe and 2% for North America over the same period[3]. Three fundamental drivers cement the region’s likely continued rise in global significance.

-

Domestic private consumption growth: India and the six most advanced economies in the Association of Southeast Asian Nations (ASEAN-6)[4] will be leaders for private consumption growth over the next decade, due to a burgeoning middle class and growing disposable income. Domestic consumption is projected to grow by approximately 6-9.5% compound annual growth rate (CAGR) compared to approximately 3.5% CAGR across the EU and approximately 4.5% CAGR within the US for the same period[5].

-

Labour productivity growth: Levels are already double that of the US and EU, compounding the APAC growth story. This is expected to improve quality of life by raising GDP per capita for more than 100 million people in developing countries across APAC, further growing the capacity of local markets to consume local goods.

-

Foreign direct investment (FDI) inflows: ASEAN has grown from being approximately 8% of global FDI flows in 2010 to approximately 15% of global FDI flows in 2025[6]. ASEAN is receiving outsized attention on the global stage, with FDI inflows into the region increasing by 8% in 2024, at a time when global flows are declining by 11%. According to joint UN and ASEAN research, much of these flows are associated with new projects, rather than being reinvested earnings flowing across borders from foreign affiliates[7]. We believe this points to a growing trend towards increased economic returns, as well as socio-economic benefits.

Why APAC private credit

Beyond the APAC growth story, a confluence of factors support the argument that APAC private credit’s decade is here. We believe these four factors – two demand-side, two supply-side – will continue to shape the next decade of the sector’s evolution.

1 - Structural credit gaps in the bank lending market

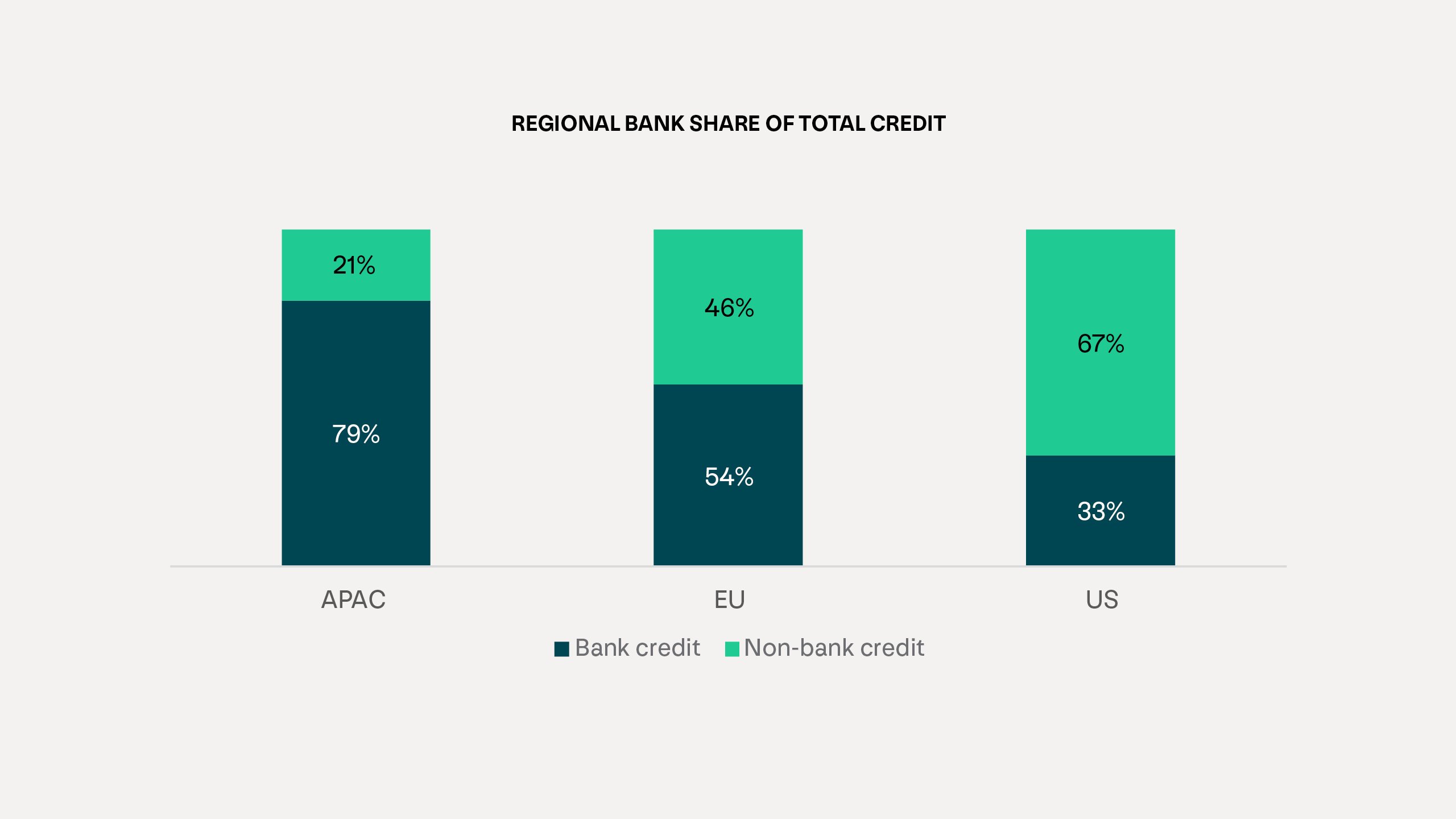

Traditional bank lending dominates the Asian and broader APAC market, accounting for 79% of corporate loans compared to approximately 33% in the US and 54% in the EU, a figure that rises even further in favour of bank lending in other segments[8]. However, the reliance on banks varies starkly from country to country, reflecting how investors must consider each jurisdiction on its own merits, considering its maturity.

At the same time, APAC banks have become increasingly constrained by regulatory capital requirements and conservative underwriting. The market also remains highly bifurcated creating significant inefficiencies for businesses that increasingly seek to capitalise on greater regional integration and rising cross-border trade.

Figure 2 – Regional bank share of total credit

Source: Bank for International Settlements. Data as at 31 March 2023

The adoption of Basel III and Basel IV by APAC banks has resulted in strategic shifts in business models. The profitability of business lines that consume high amounts of capital, such as unrated corporate and mid-market lending or specialised lending – incorporating shipping and aviation credit as well as infrastructure HoldCo financing – are being re-evaluated, with final hold appetite expected to shrink. Private credit providers are ideally placed to bridge the gap and capitalise on liquidity pullbacks in such products.

2 - Growing infrastructure, digitisation and capital investment needs strengthen demand for flexible and tailored solutions

We believe that APAC’s burgeoning middle class and domestic consumption growth sets the stage for strong investment in the wider infrastructure, consumer, communications, education and healthcare sectors, as well as presenting potential opportunities for growth in the next generation of technology.

The complexities of financing such incremental infrastructure and digitisation needs in developing countries are suboptimal from a capital perspective for traditional financiers. Consequently, critical projects may be delayed for years.

Arguably, private lenders, valued for structuring flexibility and bespoke solutions, are well-positioned to provide capital solutions to complex projects that traditional bank lenders may avoid, and may result in a win-win outcome: the potential for a positive economic return for investors and benefit to society.

3. Underdeveloped public markets and liquidity pools

Public markets in APAC lag behind western counterparts. In Asia specifically, only around 14% of corporate financing is raised via the bond market[9], compared to 64% in the US[10]. The lack of significant public market liquidity translates to a structurally significant private financing market that transfers market power to lenders with better pricing and terms.

Furthermore, from an investor perspective, tapping into the APAC growth story is not straightforward, with public markets remaining underdeveloped. In APAC, approximately 38,000 companies are publicly listed compared with around 157 million privately owned companies. As a result, we believe investing in APAC private credit is a compelling avenue to access the APAC growth story, which presents a distinct opportunity and lower-risk entry point into the region, benefitting from the upside of emerging markets, but also exposure to developed economies.

4. APAC is likely to benefit from the shift towards the multi polar order and increased focus on diversification from capital owners

Institutional investors across the globe are reassessing their portfolio allocation in light of the increase in volatility and policy uncertainties in major markets. Sentiment already indicates the intention to de risk and direct a marginal allocation to asset classes which offer greater diversification.

There are two key diversifiers in a global portfolio: geographical diversification and public/private diversification. APAC private credit arguably sits in a sweet spot where it is expected to see outsized benefits as the region is underweight in most global portfolios. It accounts for approximately 40% of global GDP and approximately 52% of global GDP growth over the past decade[11], yet receives an average allocation of approximately 4.5% from global fund portfolios[12].

Institutional investors are also increasingly allocating to private assets driven by the search for higher yields, lower volatility and diversification, with nearly half of respondents to the Private Markets 700 survey conducted by IFM Investors highlighting the asset class’s diversification and inflation hedge characteristics as attractive[13]. Acknowledging the potential benefits of committing to private markets long term, 39% of respondents also highlighted the illiquidity premium as one of the reasons private markets were attractive.

Conclusion

APAC private credit has historically provided investors with stable returns and robust growth since the Global Financial Crisis. Yet today it remains in the nascent stages of development. Structurally underpenetrated, combined with a pullback in banking liquidity and strong demand for flexible, bespoke financing solutions - juxtaposed against a backdrop of one of the fastest‑growing regions globally.

We believe APAC can provide room for growth without overcrowding, dilution of terms or going further down the risk curve to sustain returns.

The expected growth in the APAC private credit opportunity is being driven by a structural mismatch between demand and supply of capital, good economic fundamentals, and potentially robust risk-adjusted returns relative to alternatives — all within an evolving and underpenetrated financial ecosystem that may offer diversification benefits.

Partnering with managers who have regional experience, tested underwriting methodologies, extensive local knowledge and diversified, full-spectrum credit strategies is, in our opinion, the most efficient way to access this opportunity.

The key to sustainable, through-the-cycle private credit returns is the application of disciplined lending standards across a broad opportunity set. We believe APAC private credit can provide a means of generating high yield-based returns for investors willing to look beyond the familiar.

For full details, including all disclaimers applicable, please refer to the complete article.

[1] Jiri Krol, Ester Chow, Ivan Au (2025), ‘Private Credit in Asia 2.0’, p.6

[2] International Monetary Fund (2025), ‘Regional Economic Outlook Asia and Pacific: Navigating Trade Headwinds and Rebalancing Growth’, p.1

[3] Ibid, p.11

[4] Comprises Indonesia, Thailand, Singapore, Malaysia, Vietnam and the Philippines, the six most developed nations within the Association of Southeast Asian Nations.

[5] Hugo Texier (2024), ‘Unraveling Asia’s complex consumer landscape’

[6] UN Trade & Development (2025), ‘ASEAN Investment Report 2025: Foreign direct investment and supply chain development’, p.19

[7] Ibid, p.19

[8] Jiri Krol, Ester Chow, Ivan Au (2025), ‘Private Credit in Asia 2.0’, p.26

[9] OECD (2025), ‘Asia Capital Markets Report 2025’, p.10

[10] Ibid, p83

[11] International Monetary Fund data

[12] Preqin data

[13] IFM Investors (2025), 'Private Markets 700: An era of expanding possibilities', p.8

Meet the authors

Hiran Wanigasekera

Hiran is an Executive Director and Co-Head of IFM Investors' APAC Diversified Credit capability. He responsible for joint management of key credit portfolios, credit product strategies and managing the day-to-day running of debt portfolios. Hiran has worked across a wide range of credit sectors and industries including bank lending, corporate credit and structured investments.

Hong Ern Lee

Hong Ern is responsible for managing IFM Investors’ diversified credit investments in Asia, including sourcing, underwriting and structuring of private credit transactions spanning direct lending, special situations, securitizations and asset-backed lending.

Related articles

Unlocking value in mid-market infrastructure

Envisaging and enabling cities of the future

Private credit under pressure, but opportunities still exist