Key takeaways

-

Cities are under mounting pressure from accelerating urbanisation, ageing infrastructure, rising demand and decarbonisation goals. But many cities may find major overhauls to be too costly and time-consuming.

-

Increasingly, cities are likely to instead look for cheaper, incremental and modular upgrades to improve the resilience of their key infrastructure, particularly in energy, water and mobility systems.

-

Private investment can work with public bodies to implement these upgrades, enhancing the efficiency of existing systems and helping authorities identify specific areas in urgent need of overhaul.

Great cities are not static; they constantly change and take the world with them.

So said Edward Glaeser, an American economist and influential urban expert at Harvard University1. Glaeser’s work has illuminated the ways in which cities could be humanity’s greatest invention and how their evolution can have cultural and economic impacts far beyond their immediate locations.

We believe the importance of metropolises will rise even further in the coming decades, as the world’s population continues to urbanise. But so will the pressures they face. Cities will have to grapple with ageing assets, binding fiscal constraints, and decarbonisation ambitions.

Increasingly, governments appear to be recognising these challenges. However, grand narratives about the need for transformative change to modernise today’s metropolises – punctuated by system change and futuristic mobility mediums – often thinly veneer difficulties with delivery capacity and policy follow‑through. Major rehauls to existing infrastructure are simply too demanding of resources, both monetary and temporal.

Instead, the investable pathway for most cities is likely to emerge through incremental, modular upgrades that improve reliability and enhance system resilience. These changes should allow cities to better handle their growing pains and help make tomorrow’s economies more robust.

Grand narratives about the need for transformative change to modernise today’s metropolises often thinly veneer difficulties with delivery capacity and policy follow‑through.

Context and constraints

Today, 58% of the global population is concentrated in urban areas; a number expected to rise by 10% by 2050.2 This means cities will have to accommodate hundreds of millions of additional residents occupying their boundaries in the coming decades, amplifying pressures on energy, water and mobility systems.

This is causing growing stress on the infrastructure of cities. A study quantifying hourly building energy use in 277 urban areas across the US projects that energy use intensity from electricity will increase by 11.9–25.6% by 2050, compared with 2010–2019 levels.3 It is also estimated that water usage in cities will double by 2050 compared to 2021 levels.

This trend is present globally. It has prompted the UK to endeavour to bring forward a £104 billion investment plan to reduce sewer spills and water leaks and Australia to double its spend on water utilities by 2027 compared to 2023.4 Challenges in mobility are similarly costly, with London embarking on a £5.4 billion investment to transform the oldest parts of the London Underground network to future-proof the system, which typically handles over 1 billion passengers annually.

Enabling legacy networks (such as the London Underground) and new-build networks alike is capital intensive, particularly when considering decarbonisation ambitions. The IEA estimates global grids will require ~$600 billion in spend annually to keep pace with net-zero and demand growth, much of which will concentrate on urban nodes as their populations swell.5

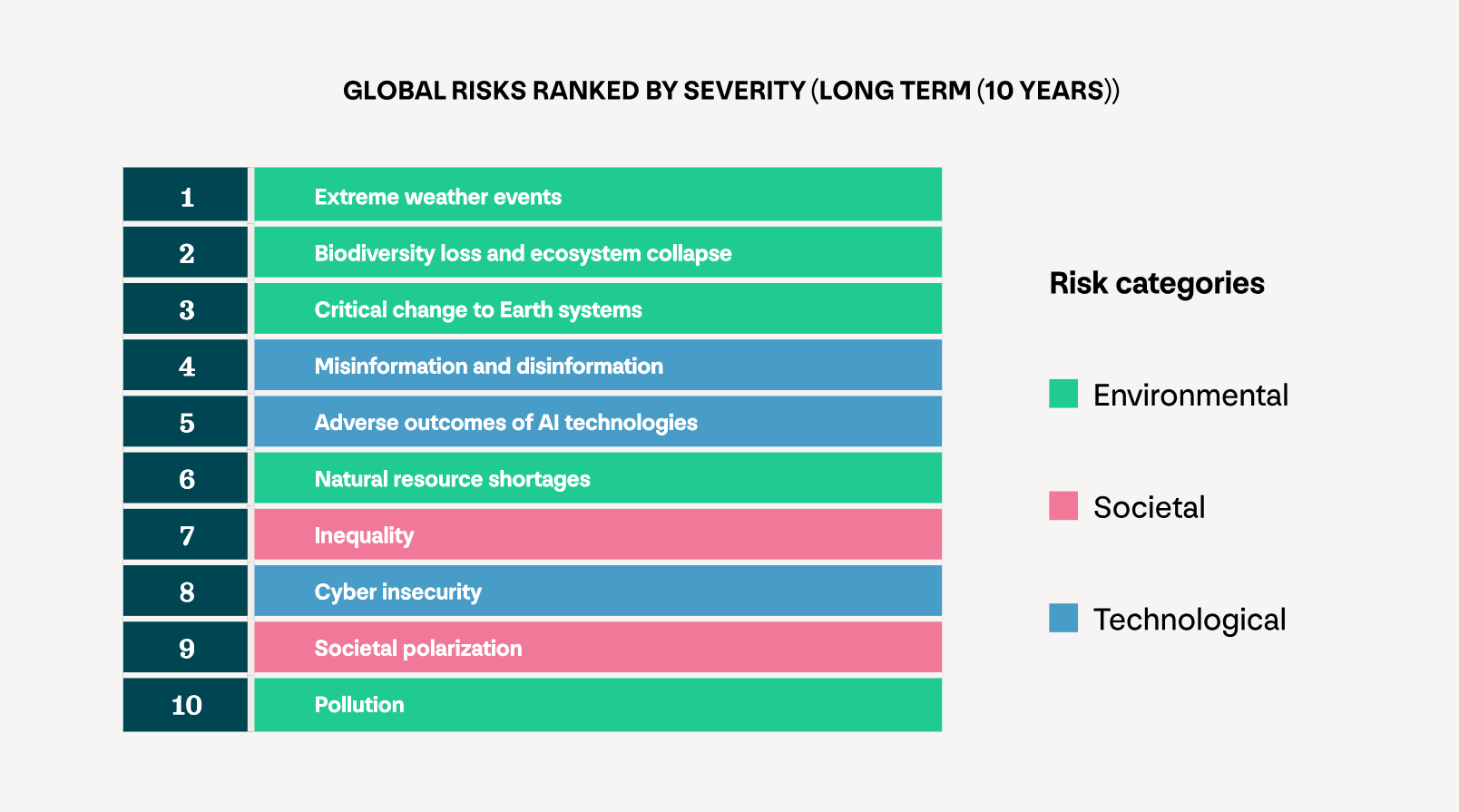

The costs of retroactively addressing the damage of climate disasters would likely prove even more exorbitant. In 2025 alone, global natural disaster losses reached approximately $224 billion, of which only $108 billion was insured.6 The World Economic Forum’s most recent Global Risks Perception Survey highlighted the looming costs of climate disaster, showing that five of the top ten global risks ranked by severity in the long term were environmental, with extreme weather events ranking as the top risk.

With or without climate change, adapting urban areas to meet the moment is likely to be frictional. Permitting difficulties, supply chain inefficiencies and skilled labour scarcity can often distort timelines and inflate project costs, even as public balance sheets face increasing constraints.

The case for incrementalism

Despite the challenges, we believe a series of incremental changes are not only possible, but increasingly necessary. Here, we focus on three areas of incremental opportunity: energy, water and mobility.

We believe a series of operative levers can help smoothen and scale energy distribution in urban settings.

Specifically, distributed energy resources (DER) can offer solutions like behind-the-meter storage to shave customer peaks and support feeder constraint7; solar PV + storage can smooth the “duck curve” (i.e. the mismatch between when solar power is generated and when electricity is needed)8; and virtual power plants (VPPs) can aggregate thousands of small assets to deliver firm, dispatchable capacity during peak windows.9

DER adoption has the potential to transform passive consumers into “prosumers”: consumers who generate, store, and flex their own energy. This can be achieved via solar PV, battery energy storage systems (BESS), electrical vehicle charging and smart meters.

Encouraging greater individual engagement can have a particularly meaningful impact in areas where demand is more concentrated. These activities can also generate tremendous volumes of data on usage patterns, which can be harnessed to better optimise energy generation.

Utilities and aggregators can leverage such data to encourage load reduction via demand side response (DSR) using real-time sensing, analytics, and remote control to manage flexible assets at scale and in partnership with users. We believe DSR offers an elegant solution to drive efficiencies in cities’ evolving energy landscapes. By temporarily reducing electricity consumption in buildings and industrial sites, it helps balance supply and demand, which reduces load and decreases grid congestion. This reduces the need for inefficient and expensive peaker plants, promotes grid stability and can provide cost savings for consumers.

French demand response and flexibility company Voltalis has established itself as a European leader in DSR. It has connected more than 1.5 million DSR devices in eight countries across Europe. These sort of solutions are most effective in jurisdictions that source electricity from renewables.

The UK offers one example. The country has a Clean Power 2030 Action Plan that seeks to source 80%-84% of its electricity from offshore and onshore wind and solar energy by 2030.10 Its grid will require flexibility to avoid blackouts and price volatility. Companies like Voltalis can help manage load variability, with the potential to harness up to 16 GW of flexible load in the UK by 2050, representing ~25% of today’s peak UK power demand.11

Another way to optimise urban energy systems is through the widespread utilisation of BESS, which also can help reduce emissions and avoid megaproject risk and costs when deployed effectively. Battery systems can draw power when supply exceeds demand and then release it during peak demand periods, such as late afternoon and early evening. Like DSR, this can help to reduce the risk of grid crashes.

BESS installation is increasing in Europe at pace, with SolarPower Europe analysis reporting that 21.9 GWh of new BESS was installed in 2024, the eleventh consecutive year of growth, bringing total battery storage capacity to 61.1 GWh.12 With continued expansion, total capacity could reach nearly 120 GWh by 2029.

Cities have similar opportunities to employ monitoring systems that improve the efficiency of their water systems.

In the UK, the Environment Agency predicts that water demand is projected to exceed current supply by over 25% by 2050.13 One of the ways to combat this is by tackling leakage. According to a report by the UK’s Department for Environmental Food & Rural Affairs, it is estimated that over 2.5 billion litres of water leak every day in England.14 The UK water regulator, Ofwat, puts this into context, estimating that around a fifth of water running through pipes is lost to leakage.15

Ofwat has embarked on an initiative with water companies to halve leakage by 2050 by imposing economic penalties on utilities that fail to demonstrate progress. Smart water meters facilitate this initiative – enabling better visibility to where and when leaks take place.

Some smart meter companies are partnering with local authorities and water utilities, using digital services to help identify leaks in real time and enable households to better understand consumption behaviour. Improved data analysis and broader smart meter adoption are supporting regulatory efforts to cut water leakages in the UK by 17% by 2029.16

While approaches to urban mobility vary around the world, many prioritise safer, cleaner and more inclusive transport systems.

To do so, they focus on multimodal integration, people-centered design, and electrification, shifting trips from private cars to public transit, walking and cycling. Digital platforms, EV adoption and improved public spaces typically support these goals.

Some densely populated areas have elected to combine bans or additional charges on internal combustion engine (ICE) vehicles with infrastructure to encourage low-emission alternatives like bicycles, electric vehicles, and electrified public transportation. For example, schemes disincentivising “gas-guzzling” vehicles offer benefits in both London and New York, promoting air quality improvement as the number of ICE vehicles in city centres drops and allowing both municipalities to raise revenue from congestion charges.

Cycling and light‑rail investments, meanwhile, can complement existing public transport. Copenhagen offers a replicable model. It has created dedicated bike lanes and "superhighways”, which integrate seamlessly with public transport, placing major bike‑parking hubs near stations and creating fluid interchanges. As a result, between 2021 and 2023 cycling made up close to half of all commuting trips in the city.17

Other cities are adopting similar models, some in partnership with Inurba Mobility, a leading European operator of public bike‑sharing and micro‑mobility services. Inurba has begun delivering tailored, technology‑enabled cycling systems across cities in Europe and Latin America to support more sustainable urban transport.

As cities revise mobility strategies, they must consider sequencing: pricing should align with credible alternatives to avoid distorted social outcomes.

Private capital appears to be well-suited to provide flexible, scalable investment to modernise urban infrastructure.

Incremental change

We believe disciplined sequencing (measure, optimise, then build) will determine urban infrastructure outcomes in the coming decades more than sweeping reinvention, and winning strategies will improve reliability and disrupt peak risk, informed by rich datasets.

Most public municipalities may find it difficult to tackle the challenges at hand in isolation. Rather, private capital appears to be well-suited to fill the resulting gap, providing flexible, scalable investment to modernise urban infrastructure.

Where public promises fall short due to delivery capacity, we believe investors should focus on mechanisms that protect downside. Principled, resolute capital can help build the future city by deploying resources with attention to fundamentals, policy and execution discipline.

We believe cultivating and financing the cities of the future poses a potential opportunity for infrastructure investors to leverage their expertise in capital structuring, long-term asset stewardship, multi-sector integration and more. Done right, this could constitute a future city structure that demonstrates resilience.

Through these actions, cities can continue to act as drivers of change – just as Glaeser observed.

For full details, including all disclaimers applicable to the data contained herein, please refer to the complete article.

[1] Triumph of the City, Harvard Kennedy School

[2] 68% of the world population projected to live in urban areas by 2050, says UN | United Nations

[4] https://www.water.org.uk/investing-future/pr24#:~:text=Breadcrumb,removing%20harmful%20levels%20of%20phosphorus. https://wsaa.asn.au/Common/Uploaded%20files/library/submission/WSAA%20Submission_NSW%20Pricing%20Proposal%20FINAL.pdf

[5] https://www.iea.org/reports/electricity-grids-and-secure-energy-transitions

[7] US Department of Energy, Pathways to Commercial Liftoff: Virtual Power Plants, September 2023

[8] ScienceDirect, Remote work might unlock solar PV’s potential of cracking the ‘Duck Curve’, August 2024

[9] Virtual Power Plant Partnership and RMI, Meeting Summer Peaks: The Need for Virtual Power Plants, July 2024

[10] National Energy System Operator, Clean Power 2030

[11] Voltalis, Can demand response save the UK’s energy grid?

[12] SolarPower Europe, New report: European battery storage grows 15% in 2024, EU energy storage action plan needed, May 2025

[13] Environment Agency, Meeting our Water Needs for the Next 25 Years, March 2024

[14] Department for Environment food & Rural Affairs, E8: Efficient use of water

[15] Ofwat, Leakage

[16] Ofwat, Supply and Standards, Leakage

[17] https://api.vejdirektoratet.dk/sites/default/files/2024-08/cykelfremme_A3_final_2024_2_ENG.pdf

Meet the authors

Adelaide Morphett

Adelaide is an Associate Director, Sustainability Specialist, in the Infrastructure Debt team, providing asset class sustainability expertise with a focus on due diligence, product development, reporting, and firm-wide strategic initiatives.

David Cooper

David is head of IFM Investors’ infrastructure debt business in EMEA and Australia. He and his team are charged with sourcing infrastructure debt deals and conducting credit analysis of prospective investments, as well as management and marketing IFM Investors' capability in this speciality.

Related articles

Private credit under pressure, but opportunities still exist

Where investment decisions can fall short – and why

Beyond data centres: Could fibre optic networks bridge the AI divide?