Key takeaways

1. The five Ds

Five tailwinds are underpinning infrastructure’s ability to anchor portfolios: digitisation, decarbonisation, deglobalisation, demographics, and deleveraging public finance.

2. Burgeoning investment prospects

Global infrastructure investment needs are approaching USD 106 trillion by 2040, according to McKinsey, offering an expanding array of opportunities across core assets and new capex-led projects in social, environmental, digital, industrial, and transport sectors. These projects can create value for both investors and communities alike.

3. Unique appeal

Infrastructure is set to continue as a standalone asset class. It can combine downside hedging and inflation resilience potential with clear increased return expectations versus other private market strategies.

Essential assets are evolving, linking conventional services with emerging technologies and security needs.

Bob Dylan’s enduring classic “The Times They Are a-Changin’” wasn’t just about politics or culture—it was about recognising when a new era is breaking over the horizon. It underscored the importance of identifying inflection points, when the old order fades and a new one takes form.

Infrastructure appears to be having such a moment now. An asset class that was once defined by airports, bridges, and utilities has widened into a far broader universe: digital networks, AI-driven systems, energy transition assets, and even defense-related infrastructure. In fact, what may seem distant today—next-generation space infrastructure, such as advanced satellites and orbital networks—could become an integral part of daily life sooner than most imagine. We believe infrastructure isn’t just evolving—it’s being redefined.

For investors, this shift means infrastructure is no longer simply a defensive, income-oriented allocation, but is increasingly a source of growth, innovation, and portfolio diversification. As a result, allocators are reassessing infrastructure’s role, moving beyond a core stabilizer toward a more dynamic, return-generating component within private markets portfolios.

While the sector is moving into a new era, the investment fundamentals that may have long anchored it as an asset class remain intact in the eyes of asset allocators: generally stable cash flows, long-term contracted revenues, inflation hedging and low volatility. We believe investors want to continue benefiting from these strengths, but they also see opportunity for infrastructure’s expansion. This appetite is reflected in our latest Private Markets 700 research, which shows investors targeting higher annual returns from infrastructure than at any point in its history.

As a result, allocators may need to reassess infrastructure’s role in portfolios, from allocation size and strategy mix to overall risk tolerance, to ensure positioning reflects both its defensive foundations and its expanding growth opportunity set. The three key themes we believe are leading infrastructure into the future are: the five D’s, burgeoning investment prospects, and distinct appeal.

Stability meets structural growth

Infrastructure emerged as a standalone asset class roughly three decades ago, led by pension systems in Australia and Canada seeking long-duration, inflation-linked assets capable of preserving the purchasing capacity of their assets and matching their liabilities across economic cycles. Initially defined by stable, core assets with predictable cash flows, infrastructure earned its place as a core holding of investment portfolios by consistently delivering resilience, income, and inflation hedging through multiple market cycles.

Today, these portfolio characteristics are being expanded and reinforced by powerful structural tailwinds. We believe digitisation, decarbonisation, deglobalisation, demographic change and government deleveraging—the 5 D's—are driving sustained demand for the infrastructure assets that sit at the heart of the global economy.

We believe the five D's build on infrastructure’s longstanding defensive strengths, positioning the asset class at the intersection of resilience and growth. As infrastructure plays an expanding role in supporting digitisation, decarbonisation, and deglobalisation, many investors increasingly view it as a durable source of real returns in an uncertain environment.

We believe this combination of essential services, inflation-linked revenues, and long-term capital investment—aligned with structural change—underpins rising return expectations across the sector, highlighting the potential appeal of infrastructure in today’s private markets.

The 5 D’s reshaping infrastructure

Digitisation

Decarbonisation

Deglobalisation

Demographics

Government deleveraging

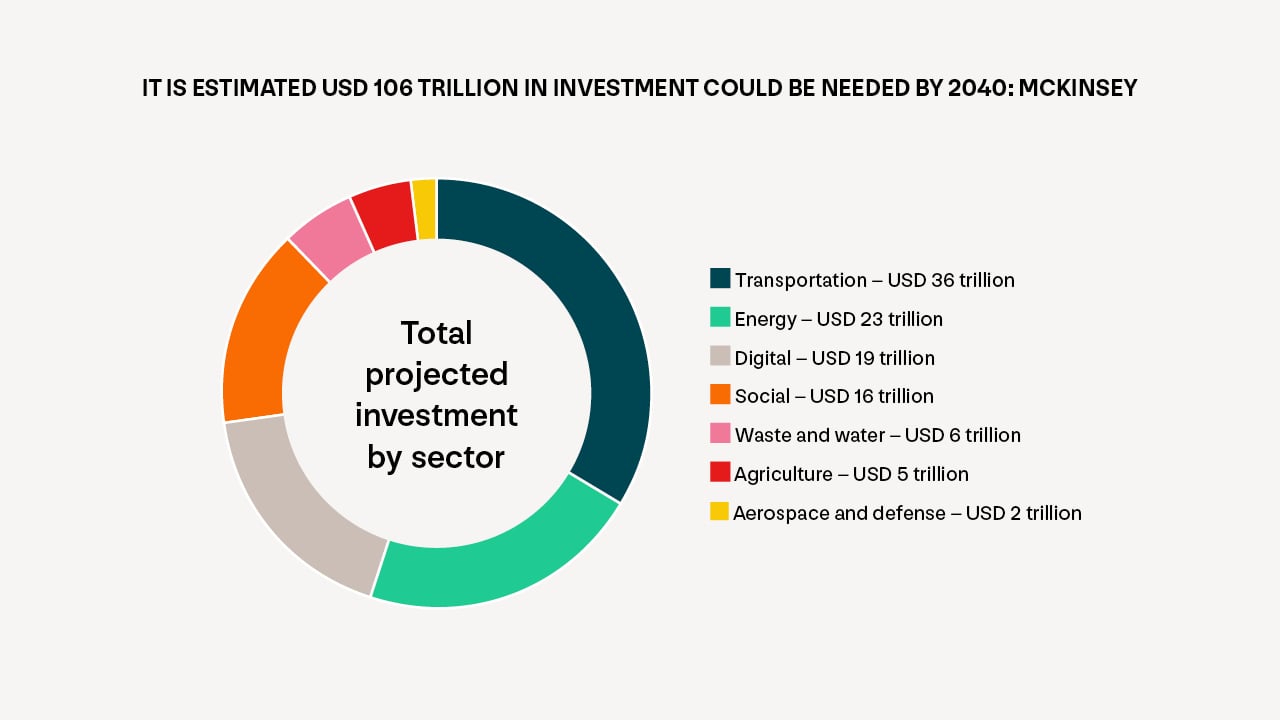

Hundred trillion-dollar opportunity

According to McKinsey, it is estimated that USD 106 trillion in investment will be necessary through 2040 to meet the need for new and updated infrastructure 1. This figure underscores the sheer scale of the challenge—and represents one of the largest, most sustained capital deployment opportunities investors have ever seen.

Much of this demand is concentrated in capital expenditure-heavy sectors, led by transportation and logistics, as cities and countries around the globe confront ageing roads, congested ports, and outdated networks. This is followed by the energy sector, which must expand overall power generation—across both conventional and renewable sources—while simultaneously upgrading ageing and increasingly strained grid infrastructure.

While much of the capital spend is expected to go toward modernising existing assets, approximately USD 19 trillion is required for digital infrastructure. This is particularly pressing. McKinsey estimates digital infrastructure will see the fastest growth in investment, as fibre networks, towers, satellites, and data centres increasingly support modern economies and the technology that power them.

Equally important, the USD 106 trillion needed isn’t just for modernisation—it’s about supporting the communities these assets serve. This capital supports essential services that people rely on every day, from reliable power and efficient transport to digital connectivity and resilient supply chains. Together, these foundations can drive economic growth, improve productivity and raise overall quality of life.

In this sense, we believe infrastructure investing can bridge long-term investor objectives with broader societal outcomes. When done well, this alignment can strengthen the social and economic fabric of the regions it serves, reinforcing trust and long-term sustainability. Put simply, it creates value for investors and communities alike.

Source: Food and Agriculture Organization; Global Infrastructure Hub; International Energy Agency; International Monetary Fund; Organisation for Economic Co-operation and Development; Preqin; United Nations; World Bank; World Economic Forum; McKinsey.

A core allocation

Infrastructure has increasingly become a standalone asset class as its investment characteristics have clearly differentiated it from other private alternatives. Once grouped with real estate or private equity, unlisted infrastructure is now recognized for its long holding periods and ability to reinvest capital over decades. These long-duration assets are generally well suited to institutional investors, particularly pension funds with long-term horizons.

This positioning is reinforced by infrastructure’s relatively low volatility, inflation hedging, and focus on essential services. Assets such as utilities, transport, and digital networks generally benefit from stable demand, regulatory frameworks, and high barriers to entry, which support predictable cash flows. Together with diversification across sectors and revenue sources, we believe these attributes bolster infrastructure’s role as a distinct and core allocation in diversified portfolios.

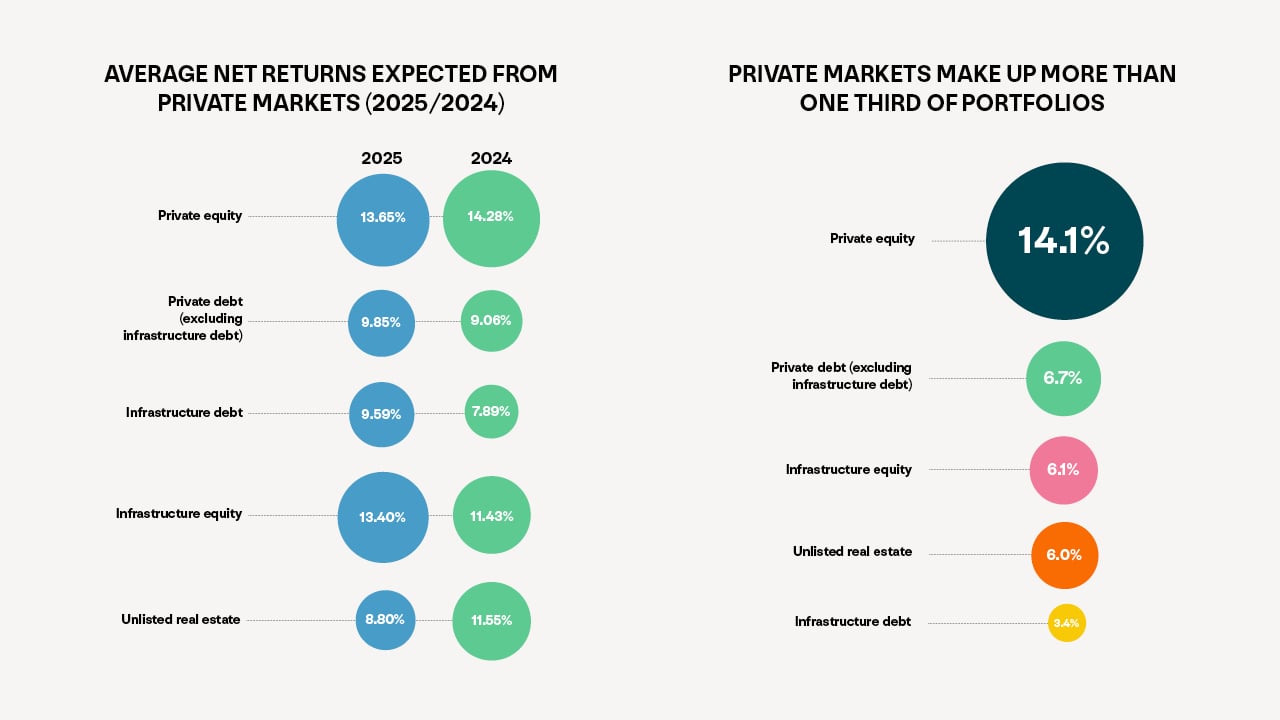

Reflecting this shift, our latest Private Markets 700 research—drawing on the views of 714 senior investment professionals across pensions, endowments, foundations, wealth managers, and leading consultants—shows investors expect stronger returns from infrastructure than ever before.

Within private markets, expected returns for infrastructure equity have risen to 13.4% in 2025, representing a nearly 200 basis point increase year-on-year—a figure now on par with private equity expected returns.

This follows increased investor interest in assets that are found higher up the risk curve, such as value-add (respondents expect 13-16% net returns), and opportunistic strategies (16%+ net return). As investors move up the risk curve, return dispersion between managers and strategies is likely to increase, reinforcing the importance of disciplined selection.

By contrast, private equity return targets remain high, according to the findings, but uncertainty around exit timing and liquidity has tempered expectations, leading to greater use of secondaries and continuation vehicles.

Source: IFM Investors' Private Markets 700, The Global Investor Barometer 2025

Return expectations for infrastructure debt have also moved meaningfully higher, increasing from 7.9% to 9.6%, which explains why allocations are expected to increase to 3.9% over the next three to five years, according to our research. This occurs as investors appear to increasingly value infrastructure debt’s ability to deliver a yield premium over corporate debt with a lower risk of loss.

Unlisted real estate, for its part, has faced even greater pressure, as ongoing challenges and structural shifts in office and commercial property markets have driven a sharp reassessment of return potential. Together, we believe these dynamics are reinforcing the relative appeal of infrastructure’s generally stable, long-duration cash flows and more predictable performance in the current cycle.

The next chapter

Infrastructure strives to align financial objectives with societal needs. As a distinct and standalone asset class, it warrants deliberate, long-term allocation within institutional portfolios. More than having the ability to deliver returns, it gives investors the opportunity to modernise the systems that form the foundation of communities and economies. We believe this asset class bridges private market ambitions with public benefit, demonstrating that generating profit and creating lasting societal value can go hand in hand.

Looking ahead, we believe infrastructure is entering a new era. Infrastructure investment now extends beyond traditional assets to energy transition, digital networks, and AI-driven systems that can help shape the economies and communities of tomorrow. As global societal needs grow, investors will have opportunities to participate in projects that deliver both financial returns and meaningful societal impact, with the goal of helping to build the systems that will sustain society for decades to come.

Against this backdrop, infrastructure warrants deliberate, long-term allocation decisions as a core strategic pillar of private markets portfolios. Indeed, The Times Are a-Changin’.

For full details, including all disclaimers applicable to the data contained herein, please refer to the complete article.

1. McKinsey: The infrastructure moment. https://www.mckinsey.com/industries/infrastructure/our-insights/the-infrastructure-moment

Meet the author

Luba Nikulina

Luba is IFM Investors' Chief Strategy Officer, responsible for leading the development of IFM’s global strategy with a focus on private markets solutions that meet the needs of Australian and global pension funds and their members. Luba joined IFM Investors from WTW, (previously known as Willis Towers Watson), where she was Global Head of Research, advising some of the world’s largest asset owners on strategy, governance and investments, managing a team of over 100 analysts. During her time at WTW, she worked in London and New York and was responsible for establishing WTW’s private markets capabilities. Luba has over 25 years of investment industry experience and has served on the UK Government’s Social Impact Investing Taskforce, City of London’s Socioeconomic Diversity Taskforce, and co-chaired the Investment Consultants Sustainability Working Group.

Related articles

Private credit under pressure, but opportunities still exist

Where investment decisions can fall short – and why

Beyond data centres: Could fibre optic networks bridge the AI divide?