Key takeaway

- For decades, the U.S. power sector operated within a stable paradigm of modest, predictable load growth. But that is shifting. A new wave of electricity demand growth is emerging, driven by AI data centers, electrification and a push for more domestic manufacturing.

-

This is creating less of a national shortage and more of a set of local bottlenecks as the grid is being asked to accommodate massive new demand in particular places on compressed timelines. In aggregate, the country can produce enough electricity. We believe the deeper problem is mismatch: the best locations for new generation are not always where demand is materialising.

-

We believe meeting the growing demand from AI data centers, electrified transport, and reindustrialisation will require significant investment. In our view, the most attractive investments sit where structural demand meets real constraints and enabling infrastructure can unlock capacity where it is currently stranded.

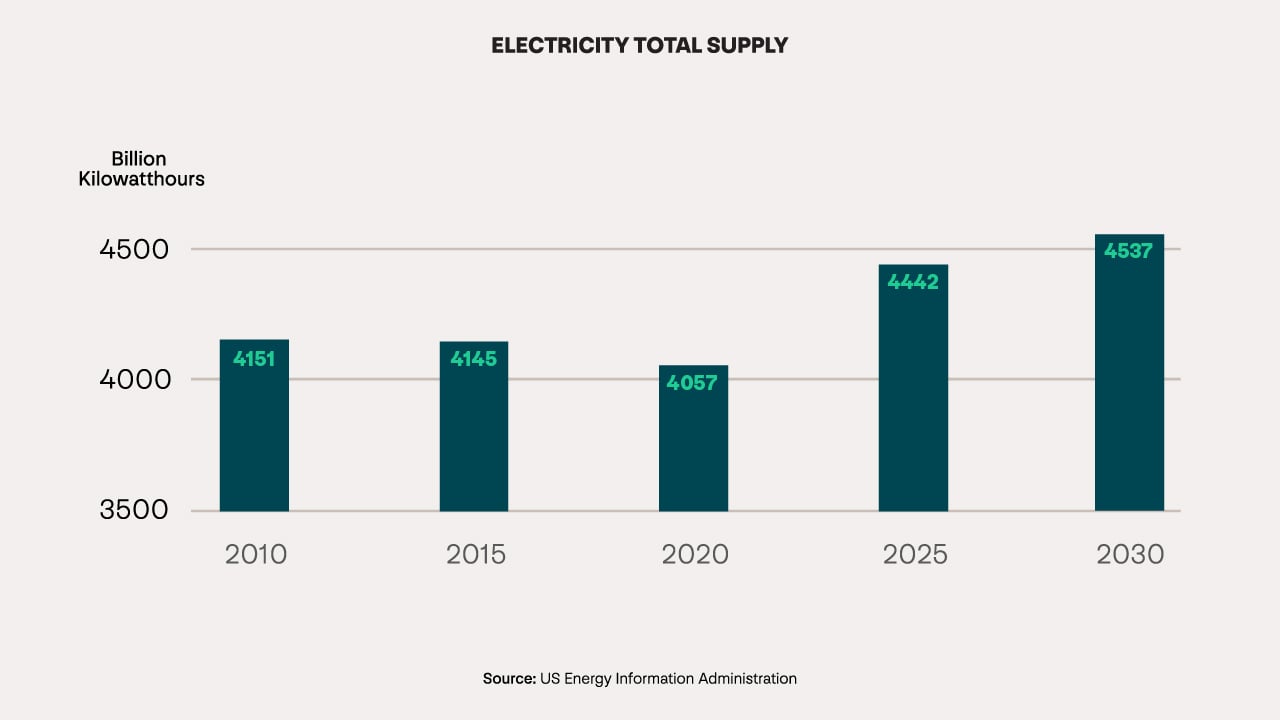

For decades, the U.S. power sector operated within a stable paradigm of modest, predictable load growth. But that is shifting. A new wave of electricity demand growth is emerging, driven by AI data centers, electrification and a push for more domestic manufacturing. This is expected to drive roughly 20% load growth between 2024 and 2030, or about 150GW of new electricity demand. This represents a rate of load growth that the sector has not seen in the past 20 years1.

We believe this shift is exposing the consequences of decisions that shaped the system over the past decade. Investment and policy focused heavily on adding renewable generation, while the capacity and footprint expansion of the grid itself have lagged. This has created a growing imbalance: generation capacity is increasing, but the infrastructure required to move that power to demand has not kept pace.

As a result, we believe the challenge is no longer just how to generate enough electricity. It is how to deliver it where and when it is needed without compromising reliability or affordability. The constraint in the U.S. power system has shifted from generation to the grid.

Chart 1 illustrates this shift in electricity supply and demand from 2010 to an estimate through 2030.

New demand moves the system from equilibrium to strain

From our observations, demand is growing in large, concentrated blocks, often with near‑continuous load profiles. It is also landing in markets faster than transmission planning, permitting, and interconnection processes today can handle. This is creating less of a national shortage and more of a set of local bottlenecks as the grid is being asked to accommodate massive new demand in particular places on compressed timelines.

The most visible example is the data center: The Electric Power Research Institute (EPRI) estimates that data centers could grow to consume up to 9% of U.S. electricity generation annually by 2030, up from 4% of total load in 20232. AI has turned compute into a large-scale industrial load: data center campuses in major markets are now planned at 300MW and increasingly, at gigawatt scale3. At the upper end of this range is equivalent to the total residential power demand of a city like Houston. These loads are arriving on 2-5 year timelines, while grid connection and network upgrades can take five years or more.

But AI is only part of the story. The system must also support the continued electrification of transport and heating, alongside new industrial demand from reshoring and advanced manufacturing. These loads behave differently and pose distinct challenges. Data centers and industrial loads are concentrated and large but predictable; transport and building heat loads are diffuse but highly variable and peaking. The grid must accommodate both simultaneously, creating an “all of the above” demand profile that is inherently complex to manage.

We believe the challenge is no longer just how to generate enough electricity. It is how to deliver it where and when it is needed without compromising reliability or affordability. The constraint in the U.S. power system has shifted from generation to the grid.

The grid must expand, but it has other levers too

In aggregate, the country can produce enough electricity. We believe the deeper problem is mismatch: the best locations for new generation are not always where demand is materialising. Transmission, storage, and system coordination are the true binding constraints.

The conversation has shifted from “Do we have enough power?” to “Can we use the system we have more efficiently?” The U.S. grid is built to meet peak demand. However, it operates well below that level most of the time. with sector capacity utilisation around 70%, implying meaningful latent capacity if the system can be used more dynamically4.

Transmission build-out remains essential, but it is slow. In parallel, more effective system coordination, including managing peak demand more actively, improving load forecasting, and integrating flexible resources that can respond to system stress, can help to unlock capacity in the near term.

In our view, storage plays a central role. It can help to absorb renewable intermittency, reduce congestion, and provide peaking support. Demand-side strategies like curtailment, load shifting, and demand response, however, are increasingly becoming important. When combined with improved day-ahead and intraday visibility and the use of behind-the-meter generation, these mechanisms can meaningfully expand the effective capacity of our existing grid. This helps bridge the gap while longer-term grid expansion takes place.

Power gets cleaner: renewables grow quickly but gas remains necessary

The supply response is becoming clearer with renewables accounting for a large share of new capacity additions, and storage scaling rapidly. However, firm, dispatchable power remains essential to system stability.

Solar and Wind

Natural gas

The infrastructure investment opportunity

New load growth necessitates new infrastructure to support it, driving multi‑year tailwinds across power generation, transmission, storage, and increasingly across adjacent systems such as transport and logistics. We believe meeting the growing demand from AI data centers, electrified transport, and reindustrialisation will require significant investment. This will span grid expansion, firm generation, storage, and the physical supply chains that underpin their delivery.

In our view, the most attractive investments sit where structural demand meets real constraints and enabling infrastructure can unlock capacity where it is currently stranded. Simultaneously, the scale and urgency of build-out are reshaping adjacent sectors such as transport and logistics and creating new sub-sectors. For example, demand response technologies like smart devices or homes are becoming critical enablers of the power system itself.

AI data centers increasingly resemble traditional infrastructure assets, providing essential services to the economy. They are supported by long-term revenues secured by investment-grade counterparties, minimal commodity risk, high margins, and operationally significant switching costs once workloads are deployed.

The resilience of infrastructure

Infrastructure that underlies and supports the real economy has demonstrated its resilience across cycles and in different growth and inflation environments. Demand for the essential services that infrastructure provides is durable; it is the defining characteristic of the asset class.

Today’s infrastructure build-driven capital cycle may be large, but it does not change the fundamental rules of disciplined investing. It requires a focus on essential services with durable, visible revenue combined with a clear understanding of cost structures, and active management of commodities and operating risks. The next phase will favor investors with deep stakeholder relationships who can navigate physical constraints and maintain capital discipline. They will also need to anchor assets in long-term, high-quality revenue streams that convert structural demand into reliable cash flow.

[2] https://www.energy.gov/oe/clean-energy-resources-meet-data-center-electricity-demand

[3] https://www.datacenters.com/news/why-100-300-mw-data-center-deals-are-becoming-the-new-standard

Lee Wright

Lee is responsible for the origination and execution of infrastructure investments, with a focus on North American digital infrastructure and freight logistics.

Related articles

Discovering growth and return opportunities across the power sector: Unlocking scalable growth in power infrastructure

Envisaging and enabling cities of the future

Beyond data centres: Could fibre optic networks bridge the AI divide?